Conjugate priors

At this point, remembering Laplace's dictum that

“probability is good sense reduced to a calculus”,

we need to model the prior in a reasonable but mathematically

convenient way.17A good compromise for this kind of problem

is the Beta probability

function, which we remind here, written

for the generic variable  and neglecting

multiplicative factors in order to focus, at this point,

on its structure:18

and neglecting

multiplicative factors in order to focus, at this point,

on its structure:18

We see that for  a uniform distribution is recovered.

An important remark is that for

a uniform distribution is recovered.

An important remark is that for  the pdf vanishes

at

the pdf vanishes

at  ; for

; for  it vanishes at

it vanishes at  . It follows

that,

if

. It follows

that,

if  and

and  are both above 1, we can see at a glance

that the function has a single maximum.

It is easy to calculate that it occurs at (`modal value')

are both above 1, we can see at a glance

that the function has a single maximum.

It is easy to calculate that it occurs at (`modal value')

Expected value and variance

( ) are

) are

In the case of uniform distribution, recovered by , we obtain the well known

E and

and

(and, obviously, there is no

single modal value).

For large

(and, obviously, there is no

single modal value).

For large  , we get

, we get

: as the values

of and increases, the

distribution becomes very narrow around

: as the values

of and increases, the

distribution becomes very narrow around  .

.

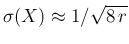

Figure:

Examples of Beta distributions.

The curves preferring small values of the generic variable ,

all having

E are obtained with (widest to narrowest)

are obtained with (widest to narrowest)

and

and  (

( : 0.16, 0.12, 0.078, 0.056).

Those preferring larger

values of ,

all having

E

: 0.16, 0.12, 0.078, 0.056).

Those preferring larger

values of ,

all having

E are obtained with (again widest to narrowest)

are obtained with (again widest to narrowest)

and

and  (: 0.087, 0.065, 0.042).

(: 0.087, 0.065, 0.042).

|

Examples, with values of and to possibly model

the priors we are interested in,

are shown in Fig. ![[*]](crossref.png) .

.

Using the Beta distribution for

, our inferential problem

is promptly solved, since

Eq. ()

becomes, besides a normalization factor and with parameters indicated

as

, our inferential problem

is promptly solved, since

Eq. ()

becomes, besides a normalization factor and with parameters indicated

as  and

and  in order to remind their role of prior parameters,

in order to remind their role of prior parameters,

So, the posterior is still a Beta distribution, with parameters

updated according to the simple rules

For this

reason the Beta is known to be the prior conjugate

of the binomial distribution. In terms of our variables,

The advantage of using the Beta prior conjugate

is self-evident, if we can choose values of and

that reasonably

model our prior belief about  . For this

reason it might be useful to invert Eq. ()

and (), thus getting

. For this

reason it might be useful to invert Eq. ()

and (), thus getting

So, for example, if we think that should be

around 0.95 with a standard uncertainty of about  ,

we get then

,

we get then

and

and  , the latter

slightly increased `by hand' to

, the latter

slightly increased `by hand' to

because our rational

prior has to assign zero probability to

because our rational

prior has to assign zero probability to  ,

that would imply the possibility of

a perfect test.19The experimental data update then

and

to

,

that would imply the possibility of

a perfect test.19The experimental data update then

and

to

and

and

.

For

.

For  we model a symmetric prior, with expected value 0.05

and

we model a symmetric prior, with expected value 0.05

and

. We just need to swap and , thus getting

. We just need to swap and , thus getting

and

and  , updated by the data

to

, updated by the data

to

and

and

. The results

are shown in Fig. .

. The results

are shown in Fig. .

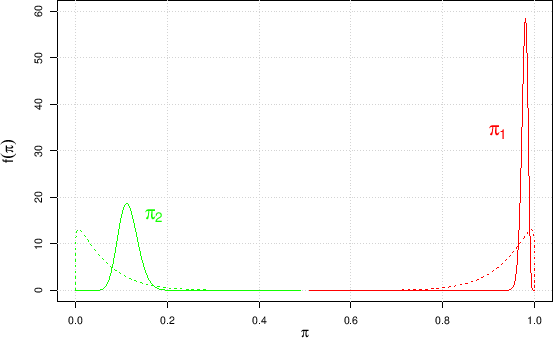

Figure:

Priors (dashed) and posterior (solid)

probability density functions

of and .

|

Expressed in terms of

expected value  standard deviation they are

standard deviation they are

As we can easily guess, using simply 0.98 and 0.12, as we have

done in the previous sections, will give essentially the same results,

in terms of expectations. Anyway, in order to be internally consistent

hereafter our reference values

will be

and

and

.20

.20